What Clark Says You Ought to Do With Your I Bonds This Yr – Cyber Tech

Sequence I financial savings bonds are one in every of cash knowledgeable Clark Howard’s favourite autos to economize and have been for a very long time.

As with many issues, you’ll should be strategic to make them work to your pockets. It is because Sequence I (“I” is for inflation) financial savings bonds reset in six-month increments primarily based on whenever you bought them. For instance, in the event you purchased an I bond in January, the speed would reset each July and January.

Make This Cash Transfer With Your Sequence I Financial savings Bond

As a result of I bonds are calculated on each a hard and fast price and variable inflation price, when issues change sufficient, your technique has to alter as effectively. And that’s why Clark says it might be time to re-buy Sequence I financial savings bonds in the event you purchased throughout a sure interval.

So that you can perceive absolutely, we’ll have to rewind the calendar a few years:

Sequence I Financial savings Bonds: How Charges Had been 2 Years In the past

In Could 2022, the Treasury Division, which points Sequence I financial savings bonds, introduced an thrilling new composite price: 9.62%. The speed was for I bonds bought from Could by means of October 2022.

“The composite price combines a 0.00% mounted price of return with the 9.62% annualized price of inflation,” the Treasury stated in a information launch on the time.

So, whereas the composite price was 9.62%, the mounted price was zero, which means you’d solely earn cash on the composite price — however what a price it was!

“There was such a frenzy shopping for these inflation bonds two years in the past when the rate of interest went to 9.62%,” Clark says, “that folks had been shopping for them in such giant numbers that the U.S. Treasury pc system crashed. It was as in the event that they had been making an attempt to purchase Taylor Swift tickets or one thing!”

Sequence I Financial savings Bonds: How Charges Are Now

Quick ahead a few years, and the scenario is totally different, Clark says.

“The latest reset dropped the inflation price that you simply’re receiving to 2.98%,” Clark says. That’s not a really aggressive price to your cash proper now when you think about:

Not all Sequence I financial savings bond house owners are taking part in these returns, Clark says.

“Individuals who purchased Sequence I financial savings bonds two years in the past, they had been incomes 9%, however at present [and] for the following six months, they’re incomes 2.98%,” Clark says. You get 2.98% whenever you subtract the 1.30% mounted price from the 4.28% composite price introduced within the newest information launch from the Treasury.

Sequence I Financial savings Bonds: Ought to You Purchase Now?

So the speed has reset to 4.28% and also you’re holding Sequence I bonds which can be solely incomes 2.98% at present. You might have a query that goes one thing like this: How are the brand new Sequence I financial savings bonds incomes greater than mine for a similar interest-earning interval?

“As a result of whenever you purchased a Sequence I bond on the cycle earlier than,” Clark says, “you had been solely receiving what was then the present price of inflation. You weren’t receiving a bonus above the speed of inflation. And that may keep the identical to your full 30 years in it.”

To place it one other manner, the reset consists of a mixed mounted curiosity and variable inflation price. The inflation price is along with the mounted price.

As talked about earlier, the speed from Could 2022 had a 0.00% mounted price. Nothing.

“Whereas someone who buys at present will get the speed of inflation plus each six months for the following 30 years they get 1.30% on an annual foundation,” Clark says. “In order that 1.30% stays the identical each six-month cycle, for the following 60 cycles — 30 years — after which they get regardless of the present inflation price is, which is calculated by the Federal Reserve.”

So, sure, if that is your scenario, Clark needs you to promote your outdated Sequence I financial savings bonds and re-buy them.

Sequence I Financial savings Bonds: What To Do With Your Outdated Bonds

Word that there’s a penalty for delivering Sequence I financial savings bonds earlier than they mature, however Clark says there’s some math that might work in your favor in the event you do the next two-fold motion:

- Promote your outdated I bond and settle for the penalty.

- Re-buy them on the new price.

Promote Your Outdated I Bond and Settle for the Penalty

“If you happen to dump the Sequence I financial savings bonds that you simply purchased inside the final 5 years, and also you bail out, you lose the final three months of curiosity. You’ll lose the annual price of two.98% or the semi-annual price of 1.49% curiosity,” Clark says. “You’ll lose that from the bond.”

Rebuy the Larger-Curiosity Incomes Financial savings Bonds

“However then you could possibly flip proper round and re-buy the bond and also you’ll make that up fairly shortly as a result of in the event you’re going to carry it for a long run shifting ahead, you’ll earn 1.3% — which you don’t with these outdated bonds — plus the speed of inflation, which is a significantly better deal,” Clark says.

To purchase Sequence I financial savings bonds on-line, go to TreasuryDirect.gov and search for the “Financial savings Bonds” tab on the homepage. Click on “Purchase a Bond” to seek out the I Bonds info.

Remaining Ideas

If you happen to’re holding onto Sequence I financial savings bonds that you simply purchased in Could 2022, they’re incomes a couple of third of what they had been on the time of buy. Clark says it’s time to promote them and re-buy new ones.

“The benefit of proudly owning the brand new ones vs. the outdated ones is so giant that you simply wish to forfeit a 90-day cycle of curiosity at at present’s decrease inflation-earning price of two.98%,” Clark says. “If you happen to forfeit that, you may then re-buy them and earn on the greater price, since you’re getting the extra 1.3%.”

Need extra money-earning suggestions? Learn our in-depth information on Sequence I financial savings bonds.

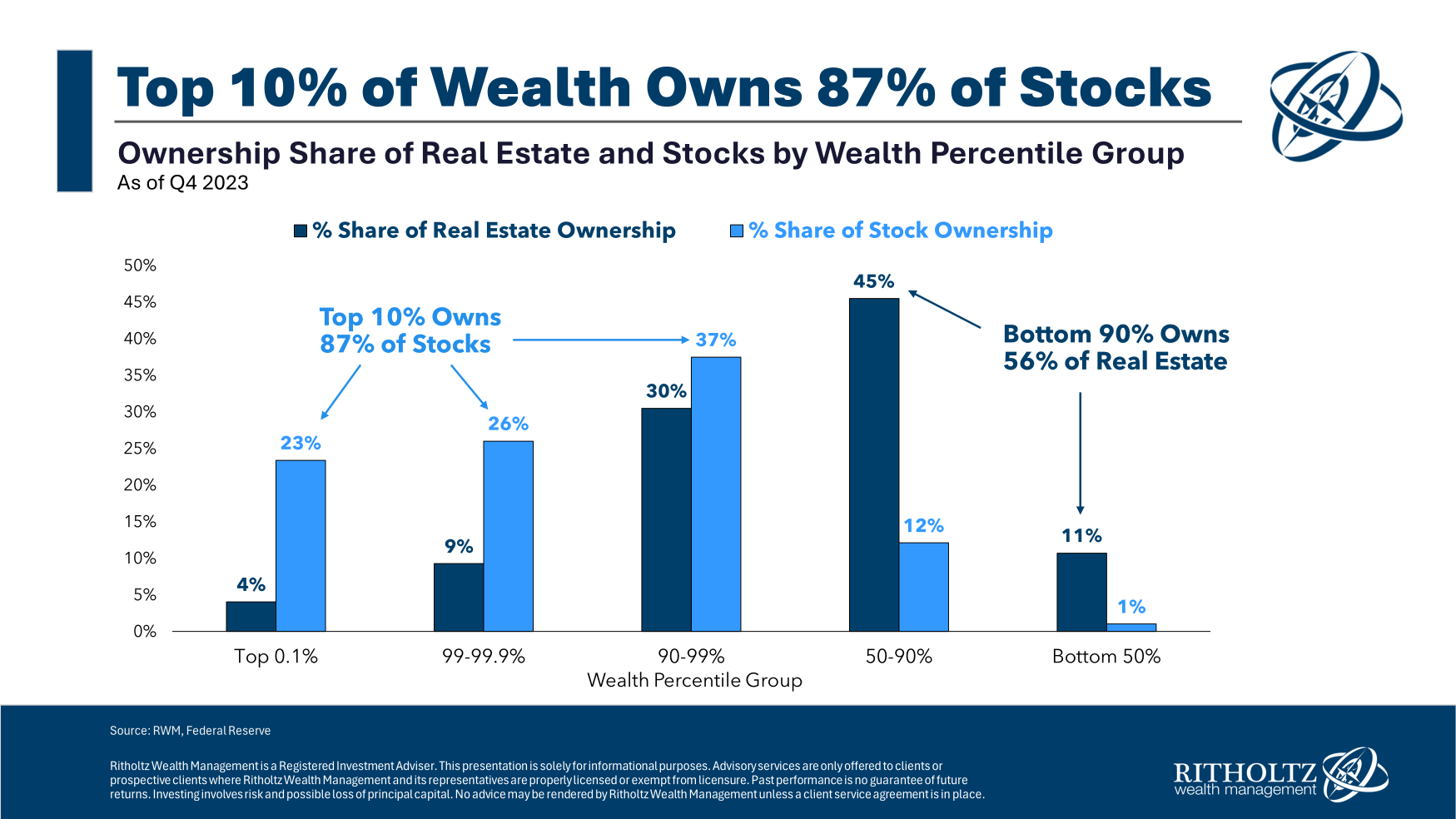

Inventory Market & Dwelling Possession Charges – Cyber Tech

Zacks Small Cap Analysis – OTC Markets Hosts Digital Investor Presentation with Jim Frakes, Interim CEO & CFO, and Steven LaRosa, MD, Chief Medical Officer, of Aethlon Medical Inc., with Marla Marin, Senior Analyst at Zacks SCR – Cyber Tech

This is What I Consider Every – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.